Abstract China's automobile industry has been through more than 60 years, from scratch, from self-reliance to joint ventures, from technology introduction to independent research and development, from foreign brands dominate the market to independent brands, until the growth of the world's first automobile manufacturing Big country, the number of possessions jumped to the top of the world...

China's automobile industry has been through more than 60 years, from scratch, from self-reliance to joint ventures, from technology introduction to independent research and development, from foreign brands dominate the market to independent brands, until the growth of the world's number one automobile manufacturing power The number of possessions has jumped to the second place in the world, and has embarked on a unique development path. Throughout China's automobile market in the past two decades, from 2001 to 2010, the national automobile production grew at an average annual rate of 24.3%, and experienced a decade of crazy growth. After entering 2010, China's auto market has entered an adjustment period. After a short period of recovery in market growth, there was another downward trend in 2014. However, the automobile industry is still higher than GDP growth and is an important engine for driving GDP.

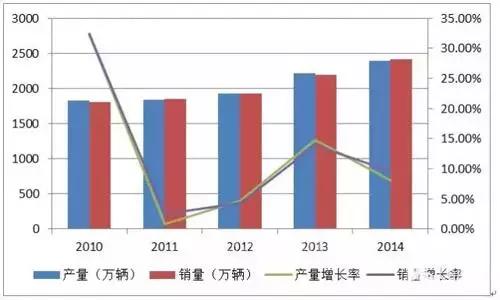

Figure 1 Automotive market data for the past five years

1 Automobile industry production and sales analysis In the first half of 2015, car sales continued to decline in the previous year, which fell to the bottom. According to data from the China Association of Automobile Manufacturers, the overall output of the automotive industry was 12.095 million units, a year-on-year increase of 2.64%, and sales volume was 11.0853 million units, up 1.43% year-on-year. Among them, passenger car production and sales were 10.327 million and 1,095,600 respectively, an increase of 6.38% and 4.80%. The total vehicle import was 531,800 units, a year-on-year decrease of 23.52%, and the export volume was 399,000 units, a year-on-year decrease of 8.94%.

Figure 2 Automotive market sales data for the first half of 2015

The world's largest auto market grew by only 1.4% compared with the same period of last year. Both imports and exports fell. The top ten automakers did not complete their sales targets. A total of 10.6391 million vehicles were sold, up 1.26% year-on-year. The industry growth rate was 0.17 percentage points. According to data from the China Circulation Association, the inventory index of China's auto dealers reached 57.3% in May this year, up 8% year-on-year, and was above the 50% warning line for 8 consecutive months. In June, the passenger car market is still not optimistic, and the decline in sales volume is a normal trend. It is expected that a new round of production and sales plan adjustments will be made. The China Automobile Association even lowered its sales growth forecast for the whole year from 8% to 3%. 2 The increase in concentration in the automotive industry has become an inevitable trend

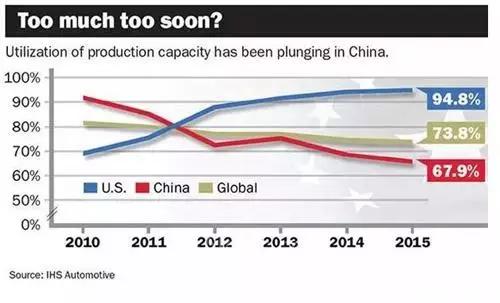

Overcapacity in the automotive industry is already a consensus in the industry. It is conservatively estimated that the production capacity of automakers in 2015 is expected to increase by 20% from the previous year to 50 million. International consulting firm IHS Automotive expects China's auto industry capacity utilization rate to be 67.9% in 2015, and Japan's media estimate is 50%, which is below the 70% capacity utilization "red light value". The rapid expansion of production capacity has also led to a decline in capacity utilization. More seriously, joint ventures and independent capacity utilization are accelerating. The capacity utilization rate of many self-owned brands is below the break-even line, both below 50%. . The capacity utilization rate of the automobile industry reaches 75%-80% to reach breakeven. It can be seen that the cost pressure of self-owned brands will continue to increase this year.

According to the "Mainstream Automaker Investment Report" issued by the Automotive Research Center of the University of Windsor, Canada, in 2012, 60% of the global vehicle production capacity was newly invested in China. From the time it is determined to invest in the construction of the plant to the start of the plant, it usually takes three years, so the capacity planning for 2012 will be concentrated in 2015. Although the growth rate of China's auto market has gradually slowed down, the investment enthusiasm of major auto companies and the expectations of local governments for capacity expansion have not subsided. At the same time as the sales target is raised, the pace of capacity expansion of car companies has also accelerated. In the past two years, there have been many new projects.

Figure 3 Estimation of China's automobile capacity utilization rate in 2015

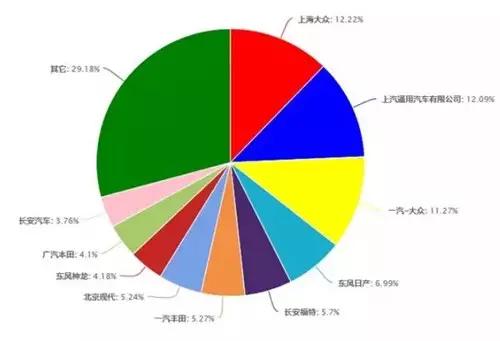

Market growth has slowed, while market concentration has increased. From January to June, the total sales volume of the top ten enterprise groups in China's automobile sales was 10.6391 million, an increase of 1.5% over the same period of the previous year, which was higher than the industry growth rate of 0.1%. It accounted for 89.8% of total car sales, up from 0.1% in the same period of last year. Taking passenger cars as an example, the market share of the top ten basic passenger vehicle companies in June 2015 was 70.82, which was higher than the 4.32 percentage points in December 2014.

Figure 4 Top 10 market share of basic passenger car companies in the first half of 2015

Against the background of sustained slowdown in the growth rate, the industry generally expects that the Chinese market is about to enter the growth inflection point, which will bring more opportunities and challenges. This kind of opportunity is conducive to further increase industrial concentration, and the development of automobile enterprises will be divided. The auto industry may face a new round of mergers and acquisitions. Xu Heyi, chairman of BAIC Group, said at the Global Automotive Forum that "China's auto market will accelerate its entry into the knockout stage. It is expected that at least 20% of domestic automakers will be out of the game by 2020, and may even reach more than 30%. A new round of mergers and acquisitions will definitely accelerate." 3 China's auto industry welcomes new opportunities in the “Belt and Roadâ€

China's auto industry is experiencing the high-speed growth of the previous period of digestion, coupled with increasing channel pressure, the future growth rate of the auto market is inevitable. However, Yao Jie, deputy secretary-general of the China Automobile Association, said in an interview with the media recently that the situation of the slowdown in the growth rate of the automobile market is consistent with the "new normal" of the economy proposed by the central government. With the introduction of China's “One Belt, One Road†new strategy, China's auto industry will usher in another round of “going out†strategic opportunities, which will not only resolve the domestic overcapacity crisis, but also achieve an industrial structure upgrade. From the perspective of corporate value, if Chinese car companies grasp the historic opportunity of the Belt and Road, successfully enter the overseas market, and consolidate their market position and brand reputation, it will become another decade or even 20 years of gold in the Chinese auto industry. Development Opportunities.

4 Analysis of China's electric vehicle market in the first half of 2015

On July 31, China Automotive Technology and Research Center released the 2015 edition of the Blue Book of New Energy Vehicles in Beijing, which is a research annual report on the development of China's new energy automobile industry.

Although China's auto market is in a special stage of sustained slowdown, China's new energy vehicle production and sales have shown explosive growth. From less than 10,000 vehicles in 2012, it reached 20,000 vehicles in 2013. In 2014, new energy vehicles broke through 80,000 vehicles. Industry experts said that 2014 is an important year for China's new energy vehicle industry development, central and local. The synergistic effect of the support policies has fully demonstrated that the production and sales of new energy vehicles have achieved rapid growth.

In the first half of 2015, the cumulative production of new energy vehicles totaled 78,500 units, a three-fold increase over the same period last year. Among them, pure electric passenger cars produced 36,300 units, a three-fold increase over the same period last year. Plug-in hybrid passenger cars produced 20,400 units, a year-on-year increase of 4 times; pure electric commercial vehicles produced 15,500 units, a year-on-year increase of 5 times. Electric hybrid commercial vehicles produced 6,406 units, a year-on-year increase of 74%. In the first half of the year, China's new energy vehicle sales exceeded the United States, becoming the world's largest market for new energy vehicles. Last year, China's new energy vehicle sales of 74,763 units, accounting for the overall market share increased from 0.08% in 2013 to 0.32%.

With the deepening of policy promotion and the clear positioning of product market, the market itself is exploding tremendous power, and the era of mass consumption of China's new energy vehicles is coming. Experts pointed out that 2015 is a year of establishing China's new energy vehicle market, with production and sales reaching more than 200,000 units.

At the same time, China's electric vehicle standard system has been further improved, and the international standard for DC charging submitted to the International Organization for Standardization has been officially released. It is the milestone event for the international coordination of automotive standards. China's new energy vehicle business model is continuously enriched and innovated, and car rental operation has become a new bright spot. The new charging business model continues to boost the scale of the industry. Power batteries and drive motors have achieved rapid development. The quality and performance of electric vehicles are becoming more mature. The types of new models are becoming more and more abundant, and consumers can choose to gradually increase. With the further improvement of the policy system, it is expected that China's new energy vehicle market will continue to maintain a high growth trend in 2015.

PVC Coated Wire

PVC coated wire is material with an additional layer of polyvinyl chloride or polyethylene on the surface of the annealed wire, galvanized wire and other materials. The coating layer is firmly and uniformly attached to the metal wire to form the features of anti-aging, anti-corrosion, anti-cracking, long life and other characteristics.

Pvc Coated Wire,Pvc Coated Coiling Wire,Big Coil Pvc Coated Wire,Small Coil Pvc Coated Wire

HENGSHUI YUZHENG IMPORT AND EXPORT CO., LTD. , https://www.yzironnails.com